")

")

")

Flash News NA 7/05/2024

Wage Garnishments - New procedures in the issuance of garnishments on the Tax Authority portal

New response procedures to wage garnishments were announced on the website of the Tax and Customs Authority during April, in order to address the reported constraints in their issuance on the portal.

What is it about?

Wage garnishment occurs as a consequence of an employee's inability to honor a specific financial obligation, whether it is towards a public entity (Tax Authority, Social Security, and other state agencies) or a private one (Banks, private service-providing companies, etc). It is a form of coercive collection aimed at reclaiming the creditor's right, realized through the judicial seizure of the employee's wages.

What are the Employer's duties?

Upon receiving notification of the garnishment, the employer must respond within the specified period and act accordingly, deducting the garnishment amount from the employee's wages monthly, in accordance with established rules, and whenever conditions permit the deduction. Subsequently, the employer must make payment to the debtor (Tax Authority, Social Security, Court, etc).

What are its limits?

According to Article 738 of the Civil Procedure Code, wage garnishment must adhere to certain rules:

• The garnishment is applied based on the employee's net wage, i.e., their earnings after legally mandatory deductions;

• The garnishable portion is specified in the notification, generally being one third or one sixth of the net wage;

• During the wage garnishment process, the non-garnishable portion may be two thirds or five sixths of the debtor's salary;

• When applying the garnishment, the employer must ensure that the employee receives at least the equivalent of the guaranteed minimum monthly wage, €820.00 in the current year;

• The garnishable amount has a maximum limit equivalent to three times the guaranteed minimum wage, thus €2,460.00 in the current year [Article 738, CPC, 2013].

How is it calculated?

Based on a net wage of €1,000.00 and adhering to the aforementioned rules, the garnishable portion would be €180.00, and the non-garnishable portion would be €820.00. One third of the considered net wage would correspond to €333.33, however, this wouldn't ensure the minimum guaranteed monthly wage. Considering a garnishable portion of €180.00 would already guarantee the national minimum wage at the current date and the remaining amount would be garnished.

What are the new procedures to be adopted in the issuance of garnishments on the Tax Authority portal?

New response procedures to garnishments were announced on the website of the Tax and Customs Authority during April, in order to address the reported constraints in their issuance on the portal.

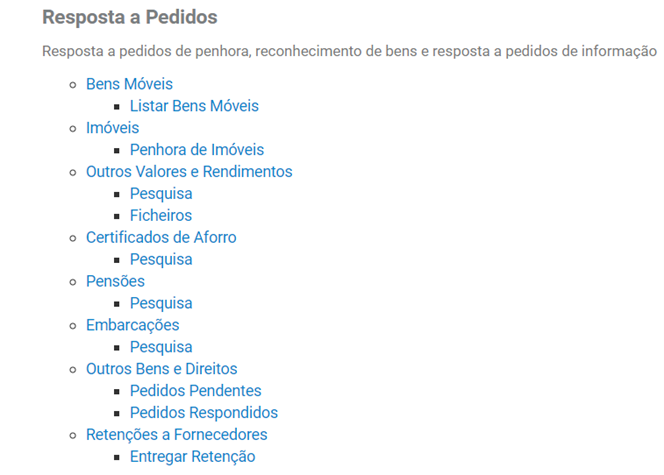

Now, to register or consult garnishments and issue payment documents, you should access the Company area, select "Services", search for "Response to requests", and in the "Response to Requests - Response to requests for garnishments, recognition of assets and response to requests for information" field, choose "Other Assets and Rights".

Check the steps below:

1.

2.

3.

4.

At Nominaurea we have specialized teams to advise and assist you in these matters.