What is Young PIT and how does it work?

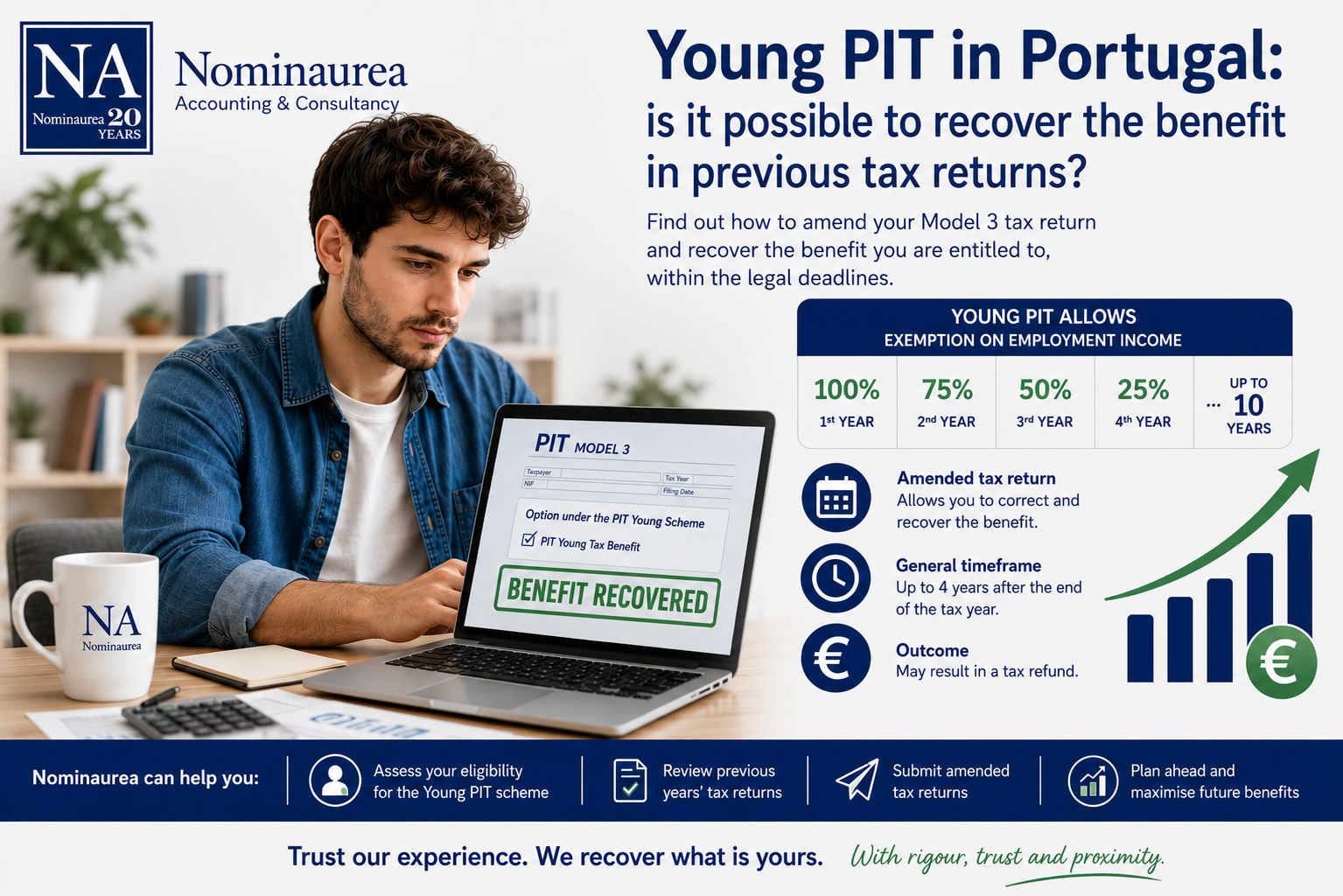

Young PIT is a tax regime that grants a total or partial exemption on employment income during the first years of professional activity, potentially covering up to 10 years and individuals up to 35 years old.

The exemption percentages are progressive, starting at 100% in the first year and gradually decreasing over time.

This benefit is not automatic: it depends on an explicit option in the tax return (Modelo 3), which explains why many taxpayers fail to activate it on time.

Is it possible to recover Young PIT in previous returns?

-

Amended returns: the general rule

Portuguese tax law allows the submission of amended tax returns to correct errors or omissions in the original filing.

In the case of Young PIT:

- It is possible to correct the return and activate the benefit if it was not initially claimed;

- The Tax Authority reassesses the tax, and a previous payment may result in a refund.

-

Deadlines to consider (critical point)

This is the main limitation:

- Up to 30 days after the legal deadline: correction without penalties

- After that: still possible, but penalties may apply

- Up to 4 years after the tax year: general deadline for review, provided the error can be corrected

👉 In practice:

For example, in 2026 a taxpayer may correct returns up to 2022 (inclusive), provided the requirements are met.

-

Latest technical interpretation

Recent technical interpretation highlights a key aspect:

- Young PIT depends on an option exercised in the tax return;

- If that option was not exercised, it may be corrected within legal deadlines;

- However, there is no unlimited right to recover benefits beyond those deadlines.

In other words, this is not a benefit that can be recovered without limits — it always depends on the legal and time framework of the correction.

-

Common practical scenarios

✔ Recent omission (within deadline)

→ Simple recovery through an amended return

✔ Previous years (up to 4 years)

→ Possible recovery, potentially with penalties

✖ More than 4 years

→ Generally no longer possible to recover

Important note

Even if the taxpayer did not use Young PIT each year, this does not restart the benefit period.

Eligibility is based on the years in which income was earned, and the taxpayer may enter directly into an intermediate benefit stage.

Conclusion

The possibility of recovering Young PIT in Portugal exists, but it is neither automatic nor unlimited.

It depends on three key factors:

- Exercising the option through an amended return

- Compliance with legal deadlines (4-year rule)

- The taxpayer’s specific situation

Acting promptly is therefore essential to avoid losing the benefit.

How Nominaurea can help

At Nominaurea, we support our clients throughout the entire tax process:

- Eligibility analysis for Young PIT

- Review of previous tax returns

- Submission of amended returns

- Tax planning to maximise future benefits

If you have doubts or believe you may have missed this benefit, we can help you recover what is rightfully yours — safely and in full compliance with the law.