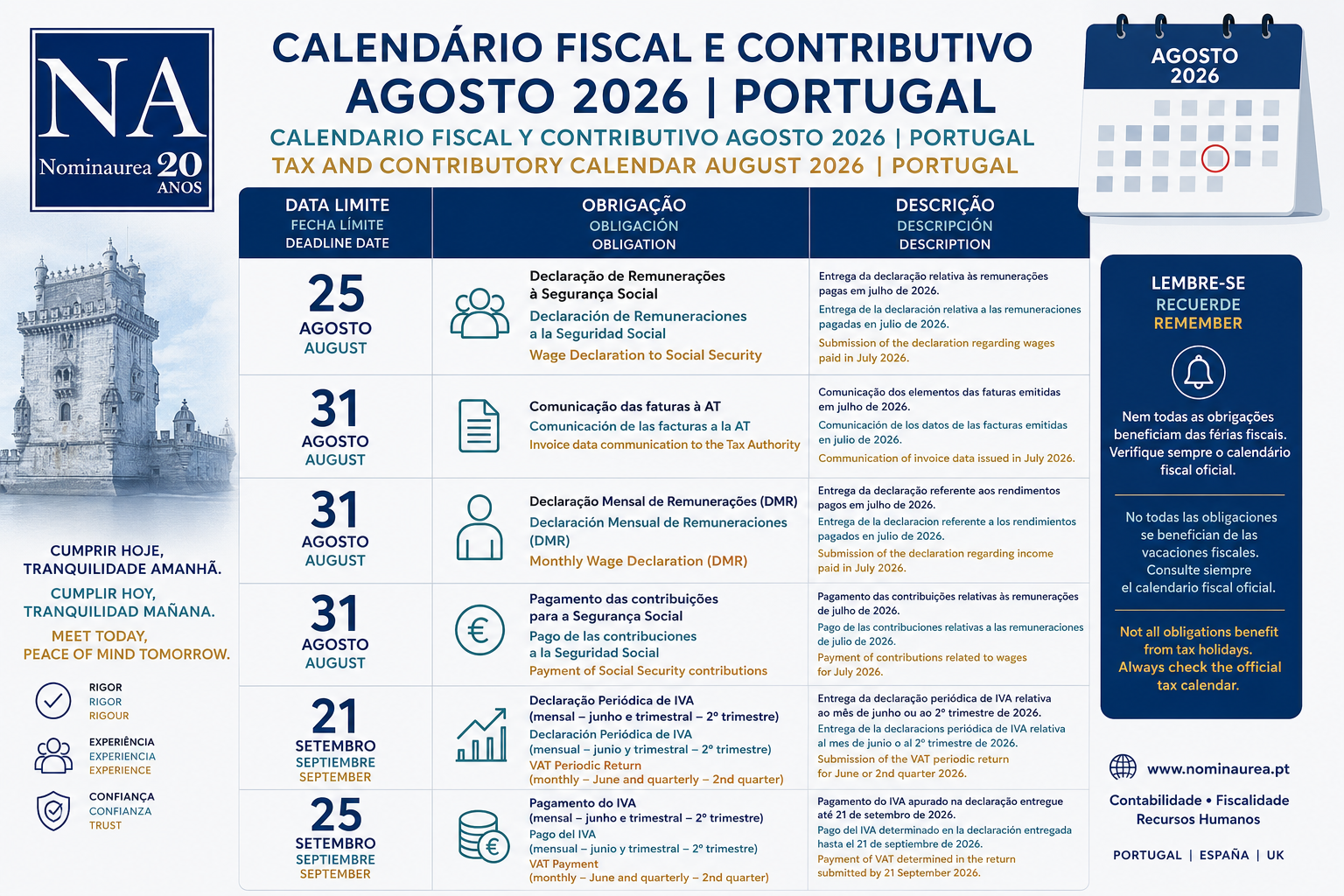

PIT Advance Payments: What Are They?

PIT advance payments are instalments of Personal Income Tax that self-employed individuals may be required to pay throughout the tax year. In practice, they work in a similar way to tax withheld at source for employees, allowing tax to be paid to the State in advance.

When the annual PIT assessment is completed, the amounts paid on account are deducted from the tax effectively due. If more tax has been paid than necessary, the taxpayer may be entitled to a refund. If the amounts paid are insufficient, the taxpayer will have to settle the difference.

Who Is Subject to PIT Advance Payments?

This obligation mainly applies to taxpayers earning income under Category B of the Portuguese PIT Code, namely self-employed workers and liberal professionals.

However, not all self-employed individuals are required to make these payments. As a general rule, an exemption applies:

- In the year the activity begins;

- In the year following the start of the activity;

- When the amount calculated for each instalment is less than €50.

The reason for this initial exemption is that the Portuguese Tax Authority uses historical data to calculate advance payments. Without a sufficient record of income and assessed tax, there is no basis on which to determine the amounts payable.

How Are PIT Advance Payments Calculated?

The calculation is carried out automatically by the Portuguese Tax Authority based on the information included in the PIT return submitted for the second preceding year.

The total amount of advance payments results from the application of a formula established by tax legislation, taking into account:

- The net tax liability of the second preceding year;

- The net income from Category B activities;

- The total net income;

- Tax withheld at source already paid.

Once calculated, the total amount is generally divided into three equal instalments to be paid throughout the year.

What Are the Payment Deadlines?

Advance payments are made on three separate dates:

- By 20 July;

- By 20 September;

- By 20 December.

The Portuguese Tax Authority usually sends a notification before each payment deadline. Nevertheless, taxpayers are advised to regularly check the Finance Portal to confirm any outstanding obligations.

Is It Possible to Reduce or Stop Paying?

Yes. Portuguese tax legislation provides situations in which taxpayers may reduce or even stop making advance payments.

This may occur when:

- Tax withheld at source and advance payments already made are sufficient to cover the estimated tax due;

- The self-employed individual ceases to earn Category B income;

- The estimated tax payable is significantly lower than the amount of advance payments calculated by the Portuguese Tax Authority.

However, this decision should be taken carefully. If reducing or suspending advance payments results in an underpayment exceeding the legal limits, compensatory interest and other penalties may apply.

Are Advance Payments Mandatory for All Self-Employed Individuals?

Not necessarily.

Many self-employed individuals are subject to withholding tax throughout the year, significantly reducing the need for advance payments. Others may qualify for exemption schemes or earn income levels that do not justify this tax obligation.

On the other hand, even where there is no legal obligation, taxpayers may choose to make voluntary advance payments, provided that each payment is at least €50. This option can help avoid a substantial tax bill when the annual PIT assessment is issued.

How Can Advance Payments Be Checked?

Self-employed individuals can consult their advance payments through the Portuguese Finance Portal, within the financial information and PIT-related transactions section.

This feature allows taxpayers to verify amounts paid, monitor potential discrepancies and obtain supporting documentation whenever necessary.

Best Practices for Efficient Tax Management

To avoid financial difficulties and unexpected tax liabilities when the annual PIT assessment is issued, self-employed individuals should:

- Regularly monitor their tax position;

- Estimate their tax liability in advance;

- Create a financial reserve for tax obligations;

- Periodically assess the need to adjust advance payments;

- Seek support from professionals specialising in accounting and taxation.

Well-planned tax management helps reduce risks, avoid penalties and improve financial control over business activities.

Conclusion

Advance payments are one of the main tax obligations for self-employed individuals in Portugal. Although they may be perceived as an additional financial burden during the year, they essentially function as a mechanism for prepaying the PIT ultimately due.

Understanding the applicable rules, calculation criteria, payment deadlines and exemption or reduction situations is essential to ensure compliance with tax obligations and avoid unnecessary costs. Regular analysis of each taxpayer’s situation allows for better-informed decisions and more effective cash flow management.

How Can Nominaurea Help?

At Nominaurea, we support self-employed individuals, business owners and liberal professionals in managing their accounting and tax obligations.

Our services include:

- Analysis of the obligation to make advance payments;

- Tailored tax planning;

- PIT simulations and tax liability estimates;

- Assistance with reducing or ceasing advance payments where legally permitted;

- Ongoing accounting and tax support;

- Clarification of issues and assistance in dealings with the Portuguese Tax Authority.

With a specialised team focused on our clients’ needs, we help transform taxation into a management tool rather than a concern.